Mortgage rates in Europe vary considerably across countries. This article walks you through the differences between European mortgage rates and explains key variables that reflect the health of European mortgage markets. It finishes with a focus on the role of foreigners in the Spanish real estate and mortgage markets.

Mortgage rates across the EU

As of early 2026, the average European mortgage rate hovered around 3.44%, with rates for new house purchases typically ranging between 3% and 4%, depending on the term. However, there is great variation across countries. Mortgage rates tend to be relatively high in Eastern Europe; high enough that they significantly raise the EU average. In early 2026, Poland had the highest mortgage rates, generally ranging between 6.5% and 9%. 5-year fixed-rate options in Poland often fall around 6.5%–7.5%, depending on the bank and deposit size. Hungarian mortgage rates for standard loans generally ranged between 6% and 8.5%, with average rates around 6.5%-7%.

On the other end of the spectrum is Bulgaria. At the end of 2025 Bulgarian mortgage rates were as low as 2.25%–2.28% for qualifying individuals.

Why mortgage rates vary across countries

It’s important to recognize that mortgage rates are not directly set by any one entity. Many people think that mortgage rates are set by the Central Bank (or Federal Reserve, in the US), but this is only part of the formula. Changes in mortgages rates arise from the complex interplay of many economic factors. Here are some of the main ones:

Interest rates

Central banks do indeed set the economy’s main interest rate. In the EU, it is the European Central Bank (ECB) that sets the overall rate. This rate trickles down to other debt instruments, such as bond yields and mortgage rates. This is because when the ECB raises rates, it becomes more expensive for banks and lenders to borrow money, which translates to increased rates for all borrowers, including those wanting to purchase homes. The converse is also true.

It’s important to note that often mortgage rates lead the policies of central banks. Financial markets are driven by investor expectations. All around the world, investors focus on the expected actions of central banks. If they expect the central bank to change interest rates, often mortgage rates will reflect these expectations.

Inflation rates

Simply put, inflation is the increase in the prices of goods and services over time. When inflation rises, it limits the purchasing power of consumers. This is a consideration lenders make when setting mortgage rates; they must adjust mortgage rates to levels that compensate for eroded purchasing power when inflation rises too quickly. This is because lenders still need to make a profit on the loans they originate, which becomes more difficult when consumers’ buying power is diminished.

Government policy

If a government implements policies that promote home ownership, it can influence mortgage rates. This is not typically the case in Europe. In the US, however, Government Sponsored Entities (GSEs) play a huge role in the mortgage market. Two agencies, the Federal National Mortgage Association (Fannie Mae) and the the Federal Home Loan Mortgage Corporation (Freddie Mac), are the main holders of US mortgage debt (they purchase the debt from lenders). This is advantageous as it leads to lower funding costs and the pooling of risks. By contrast, in the euro area, housing loans remain to a large extent on banks’ balance sheets and are mostly financed via bank deposit.

Generally, while accounting rules differ across euro area countries, loans can be less easily removed from banks’ balance sheets than in the United States. The fact that loans remain to a large extent on the balance sheet of regulated institutions, i.e. banks, tends to support a more cautious behavior of lenders with respect to the loans originated. This, combined with the fact that the US is the only country where a 30-year fixed rate mortgage is standard (a result of government policy to encourage home ownership) is one of the main differences that US mortgage rates are so different than European mortgage rates.

Summary

It’s the interplay of all the factors that cause European mortgage rates to vary across countries. It’s also the reason that European mortgage rates are so different than US interest rates.

The professionals at Madrid Estate would love to help you find and purchase your dream property in Madrid. You can contact our founder Fabiana Greci directly at fabiana@madrid-estate.com or WhatsApp +34 680 306 337 to learn how we can help with your property search and purchase.

Health of mortgage markets across the EU

Residential loans as a percentage of disposable income

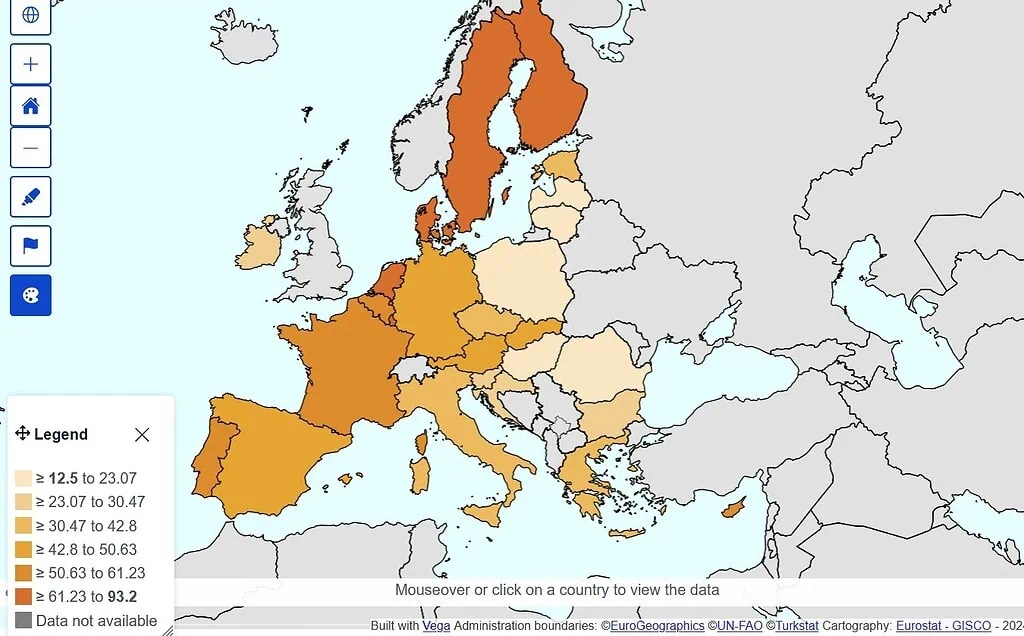

One of the most telling indicators for the health of a country’s mortgage market is household indebtedness. This represents the ratio of all outstanding debt to overall household disposable income. The ability of households to take on new debt is an important factor that influences the prices of residential properties. As of the end of 2024, The Netherlands had the highest household indebtedness in Europe, at 93.2%. The country is in the middle of a real housing crisis. As home ownership has become less affordable, demand for rental properties has surged, pushing up rental prices and creating a cycle of housing un-affordability.

Spain’s metric for household indebtedness is at 43.7%, which is below the European average.

Total value of mortgages issued to citizens

If a country has a high number of mortgages issued to its citizens, this is indicative of a very active housing market with high transaction volumes and substantial lending activity. France (740,000), Spain (381,045), the Netherlands (332,482) and Italy (303,689) have the

highest numbers of mortgages issued in Europe.

Belgium (187,516), Poland (162,375), Portugal (90,868) and Israel (73,933) exhibit moderate numbers of mortgages issued. These figures suggest a healthy level of mortgage activity, with significant but less intense lending compared to the top-tier countries.

Hungary (51,605), Czech Republic (42,608) and Ireland (35,947) have lower numbers of mortgages issued. These figures reflect smaller market sizes or possibly stricter lending criteria, resulting in fewer mortgage transactions.

Average value of mortgage issued

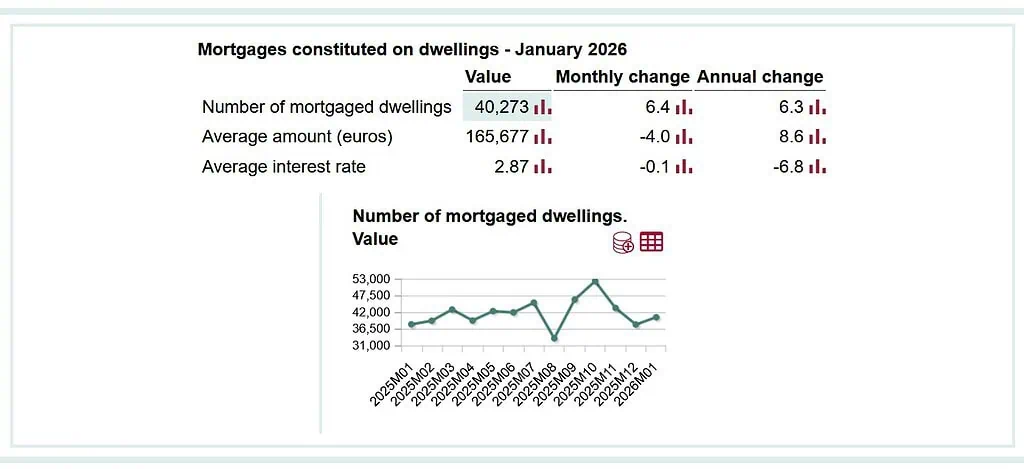

A high average value of mortgages issued in a country reflects higher property prices. This points to the existence of a premium housing market and an ability to easily finance more expensive properties. The average value of mortgage issued in Spain was 165,677€ in early 2026. This is up from142,000€ in 2023, when we initially published this article. This demonstrates the strength of the Spanish housing market as the number increased significantly even as interest rates increased. A big portion of this is due to the fact that the rise in interest rates coincided with a significant wave of migration, which is driving up sales to resident foreigners. According to CaixaBank, sales to non-resident foreign buyers account for around 44% of all sales to foreigners (cumulative data for the four quarters trailing 3Q 2024).

LTV ratios

The loan-to-value (LTV) ratio is the principal amount of a mortgage loan divided by the value of the property it financed; it is typically expressed as a percentage. The LTV ratio is a pivotal factor in mortgage lending across countries, determining how much of a property’s value lenders are willing to finance. Lower LTV ratios can lead to lower mortgage rates; this is because they reflect lower risk to lenders.

LTV ratios vary widely across Europe, due to local market conditions and regulatory frameworks. LTV ratios can be tailored to balance

risk mitigation for lenders and the ability of borrowers to buy their own homes. Spanish regulators attempt to do exactly this: different LTV limits apply based on property type. Current Spanish LTV ratios are 80% for primary residences, 70% for secondary residences, and 60% for investment properties, with government guarantees available for young people and families with dependents.

Expat Tip: The typical loan-to-value ratio for non-residents is 60 to 70 percent. Mortgage terms for expats are often capped at 20 to 25 years, rather than the 30 years available to residents.

Focus: Non-Spaniards participating in the Spanish mortgage market

As we wrote in our blog post Spanish mortgages for investors, non-Spaniards can obtain mortgages from Spanish banks. According to the Spanish Association of Property Registrars (Colegio de Registradores), sales to foreign buyers accounted for 14.9% of the total, at around 87,600 sales, in the four quarters trailing 3Q 2024. However, this represented only a small percentage of all Spanish mortgages. This highlights the growth potential of the Spanish mortgage market for foreign buyers.

Foreigners that are residents of Spain

Foreign residents tend to buy homes and take out mortgages for similar amounts as Spaniards.

Foreigners that are not residents of Spain

Spanish banks view lending to non-residents as riskier than lending to residents, thus:

- Non-residents have to pay larger down payments than residents.

- Mortgage rates for non-residents will be higher than those published for residents.

- The criteria for non-EU citizens may be different compared to those who reside in the EU.

Even though they have less favorable mortgage rates, non-resident foreigners tend to purchase significantly more expensive homes than residents, thus the average mortgage taken out by foreigners is higher.

As to be expected, there are notable differences depending on nationality and autonomous region. Alicante is the province with the most foreign buyers, where they represent approximately half of all sales, with a significant presence of non-residents (68.6% of the total number of foreigners). Other tourist provinces, such as Malaga and the Balearic Islands, also have a large proportion of non-resident foreign buyers. On the other hand, resident foreigners predominate in Barcelona, Madrid and Valencia.

Key takeaways for investors

Spain has some of the lowest mortgage rates in Europe. Due to structural differences in mortgage markets in the EU vs. the US, they are significantly lower than US mortgage rates. Most metrics of mortgage market healthiness, such as household indebtedness and LTV ratios, indicate that the Spanish mortgage market is in good condition. Although foreigners are increasingly taking advantage of the relatively low rates and healthy Spanish mortgage market, they still only represent a small percentage of all Spanish mortgages. Thus there are ample opportunities for investors to obtain mortgages from Spanish banks.

Madrid Estate has a great deal of experience helping investors obtain Spanish mortgages. We have connections with a number of mortgage brokers and can help guide you through the process of obtaining a Spanish mortgage. You can contact our founder Fabiana Greci directly at fabiana@madrid-estate.com or WhatsApp +34 680 306 337 to learn how we can help with you obtain a Spanish mortgage.